KYC 2-ways: a recipe for success

We often think financial crime is the result of criminals hacking into an organisation to steal data and in some cases, the firm’s bank accounts with financial implications. Financial crime prevention has always been a hot topic for the banks, but it is now also becoming the case for the legal sector. Criminals are becoming more sophisticated nowadays and can target unprepared organisations in ways that seem to be part of the typical client- business relationship, but using illegally obtained money to fund the relationship and launder funds. Legal professionals are key actors in the business and financial world, facilitating important transactions that underpin the UK economy. As such, they have a significant role to play in ensuring that their services are not used to further a criminal purpose. Money laundering and terrorist financing are serious threats to society, potentially leading to revenue loss, endangering life, and fuelling other illegal activity. Within the legal sector client relationships have traditionally been built on a personal one to one relationship between the senior fee- earners and the client. Nowadays, personal relationships are increasingly difficult to establish and maintain. It is therefore vital that you know with whom you are dealing. Having established the client’s credentials, understanding and knowing your client’s business will help to enhance the relationship, establish customer loyalty, and enable your firm to offer appropriate additional value-add services.

Know your Customer – Start of the relationship

We all know the process as Client Due Diligence (CDD), it’s not new, but the depth at which the checking is now mandated and the urgency to complete checks before work can start is becoming key to every law firm.

CDD may also identify the client as a Politically Exposed Person (PEP), typically politicians and celebrities. This does not mean the firm cannot accept work from the client, although additional diligence, often referred to as enhanced due diligence or EDD, must be undertaken when dealing with the client.

Traditional methods of completing CDD can be quite lengthy and not consistently executed, therefore providing incomplete and potentially incorrect results. However, these steps can now be automated using policy-driven multi-jurisdictional processes, producing consistent and accurate results in a fraction of the time compared with manual CDD procedures. This part of the discovery process should also include a thorough search of any adverse media that might exist.

Using automated systems reduces the firm’s risk. It releases valuable resources back for value add and chargeable work and gives the firm commercial advantage over its competitors; clients are entitled to expect prompt service.

Once the client’s credentials have been established, work can begin.

Once the client’s credentials have been established, work can begin. However, it doesn’t stop there. Sanctions lists are updated daily, a clients relationship with undesirable entities could change, so there is a responsibility to continually refresh your clients’ risk assessment to keep safe.

Regular screening should occur to detect changes in your clients’ profile. For example, you take on a client – all is good, but their business model changes – and so you need to refresh the CDD file. What if someone moves into bitcoin trading or legal cannabis. How would you detect this and refresh their file? This is more of a legal requirement in some countries than others, so you need to check the client’s location and source of funds, for example.

Another example might be a need to make sure your client does not breach Oil embargo trading – how would you know? You need to screen and screen at least weekly. This is far harder to do than regular money laundering cash processing checks, but the fines are far more significant.

Finally, you need to consider global relationships and global regulators. How do you police a US client who hires you in the UK but the client is subject to US rules, regulations and fines. As a UK firm, you would need to know this.

Anti-Money Laundering

Establishing the client’s validity also protects the firm from unwittingly playing a part in the laundering of illegal money.

Modern financial institutions use sophisticated Anti-Money Laundering (AML) systems to detect their clients’ unusual payments and unexpected behaviour.

Law firms are increasingly expected to recognise clients that may be using businesses to launder money and may be unwittingly involved by facilitating typical transactions such as:

- buying and selling of real property or business entities

- managing of client money, securities or other assets

- opening or management of bank, savings or securities accounts

- the organisation of contributions necessary for the creation, operation or management of companies

- creation, operation or management of trusts, companies, foundations or similar structures

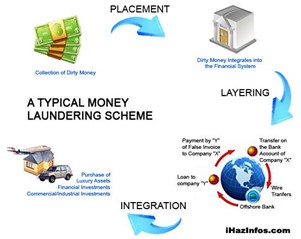

The money laundering cycle can be broken down into three distinct stages; however, it is important to remember that money laundering is a single process. The stages of money laundering include the:

- Placement Stage

- Layering Stage

- Integration Stage

- The Placement Stage

This is where the “dirty” cash or proceeds of crime enter the financial system. Generally, this stage serves two purposes: (a) it relieves the criminal of holding and guarding large amounts of bulky of cash; and (b) it places the money into the legitimate financial system.

The placement of the proceeds of crime can be done in a number of ways. For example, cash could be packed into a suitcase and smuggled to a country, or the launderer could use smurfs to defeat reporting threshold laws and avoid suspicion. Some other common methods include: Loan repayments, Gambling, Currency Smuggling and Currency Exchanges.

- The Layering Stage

After placement comes the layering stage or ‘structuring’.

The layering stage is the most complex and often entails the international movement of the funds. The primary purpose of this stage is to separate the illicit money from its source. This is done by the sophisticated layering of financial transactions that obscure the audit trail and sever the link with the original crime.

During this stage, for example, the money launderers may begin by moving funds electronically from one country to another, then divide them into investments placed in advanced financial options or overseas markets; constantly moving them to elude detection; each time, exploiting loopholes or discrepancies in legislation and taking advantage of delays in judicial or police cooperation.

- The Integration Stage

The final stage of the money laundering process is termed the integration stage.

It is at the integration stage where the money is returned to the criminal from what seem to be legitimate sources. Having been placed initially as cash and layered through a number of financial transactions, the criminal proceeds are now fully integrated into the financial system and can be used for any purpose.

There are many different ways in which the laundered money can be integrated back with the criminal; however, the major objective at this stage is to reunite the money with the criminal in a manner that does not draw attention and appears to result from a legitimate source. For example, the purchases of property, art work, jewellery, or high-end automobiles are common ways for the launderer to deploy their illegal profits without drawing attention to themselves.

Financial Action Task Force (FATF)

In response to mounting concern over money laundering, the Financial Action Task Force on Money Laundering (FATF) was established by the G-7 Summit held in Paris in 1989.

FATF regularly publishes updates on all countries’ progress in applying Financial Crime and Anti-money laundering policies.

These now extend beyond the traditional banking and financial institutions and now include monitoring of the legal sector. A recent example is: Following FATF’s Mutual Evaluation Report from April 2020 and as reported in Emirati News: Two hundred law firms had their licences suspended for a month by the UAE’s Ministry of Justice for breaching anti-money laundering regulations. The Emirati Ministry of Justice has encouraged the suspended firms to contact the Ministry in order to remediate the deficiencies.

Solicitors Regulation Authority (SRA)

A 2019 review from the SRA reported that a fifth of all law firms fail on money laundering compliance, stating:

- A fifth of firms reviewed don’t have required firm risk assessment

- 7,000 firms will be checked for compliance

- New annual Risk Outlook highlights 172 money laundering investigations this year

“In March, we wrote to 400 firms asking them to demonstrate compliance with the 2017 Money Laundering Regulations by sending their firm risk assessments. We received 400 responses, but 21 per cent (83) were not compliant. They either did not address all the risk areas required (43), or they sent over something other than a firm risk assessment (40) – for instance, a client or matter risk assessment.”

Paul Philip, SRA Chief Executive, states: “A call from us should not be the prompt for a firm to get their act together. You need to take immediate action now if you are not on top of your money laundering risks. Where we have serious concerns, we will take strong action.”

The firm received the monies from clients before any or all of the customer due diligence had been done

The SRA review goes on to say “new EU money laundering regulations are due to come into force by 10 January 2020. This will mean firms need to update their processes to bring them up to date with the new legislation.”, which could lead to a massive spike in activity for your KYC teams. The SRA’s #staySHARP campaign is all about raising awareness of the threat money laundering poses to the legal sector. That means staying SHARP – solicitors SHould Assess, Report, Protect.

- Assess: Firms need to assess their risk – that means having an adequate firm-wide, money laundering risk assessment policy.

- Report: if a solicitor suspects a client or transaction might be using the proceeds of crime, they must report this to the National Crime Agency by submitting a Suspicious Activity Report (SAR).

- Protect: make sure your staff understand the risk money laundering poses, are familiar with the firm’s risk assessment policy and process, and are effectively working to keep your business safe.

The SRA has also started to impose fines for non-compliance: As reported by LegalFutures: In September 2020 it was reported that law firm Taylor Vinters had been fined by the Solicitors Regulation Authority (SRA) for failing to undertake proper money laundering checks on millions of pounds paid into its client account.

The firm received the monies from clients before any or all of the customer due diligence had been done.

The agreement said: “The firm did not know who had provided the clients with its bank details. Once the firm became aware, it informed clients not to send funds until the required customer due diligence had been completed.”

Know your Customer – Building and extending the relationship

Clients are easy to find and hard to keep. Maintaining client loyalty is becoming hard work. Law firms are increasingly turning to data to understand the client’s business and strategic goals for the future. This is where the forward-thinking firms can build a ‘trusted advisor’ relationship with the client. Actively providing additional non-legal services, where the law firm can add value and help the client achieve it’s strategic goals.

These may be in areas where the client would not expect the firm to have expertise. But in order to provide appropriate services you need to Understand and Know Your Customer’s business.

Summary

In summary, KYC 2-ways is a good thing:

1. To avoid reputational risk and or penalties, you must be sure that you are dealing with reputable clients.

2. In today’s market, you must know even more about your clients and their business goals to secure client loyalty and grow the number of services that your firm can provide.

The Databilities team have over 60 years of experience delivering advice and solutions into the Banking and Legal sectors working on global programmes to improve financial crime threat mitigation and reduce the potential for money laundering.

Databilities can advise on the latest solutions to improve your CDD/KYC processes, reducing risk, cost and time to complete the process.

Credits

This article was written and edited by Brian Jones, Chris Wotton and Paul Caden at Databilities.

With additional contributions from

1. Solicitors Regulation Authority

2. Anti-Money Laundering Guidance for the Legal Sector

3. LegalFutures

4. Emirati News

5. Heather Webster

For more information please contact Databilities:

Email: info@databilities.co.uk

Web: https://databilities.co.uk

For more articles in the Databilities ‘It’s all in the data…” series follow us on LinkedIn